Choosing the Right Mortgage Term: 15-Year vs. 30-Year Loans

When you’re purchasing a home, every decision matters—from finding the perfect property to selecting the financing option that best supports your goals. One of the most important choices you’ll make is the length of your mortgage term.

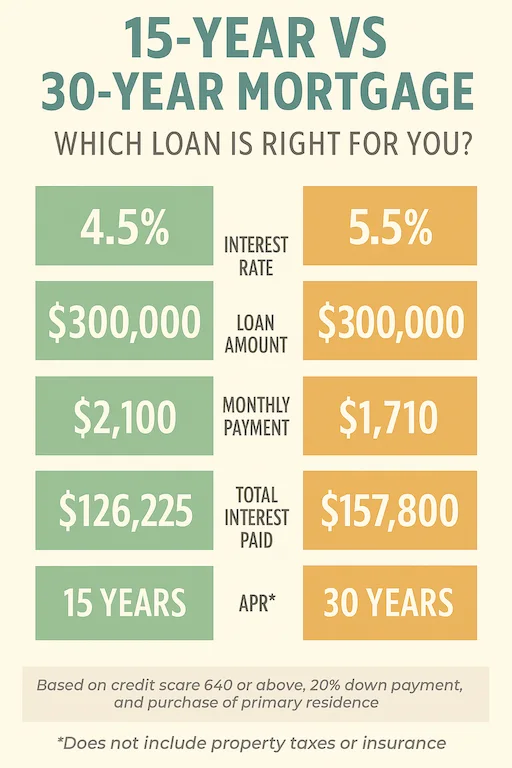

For most homebuyers, the decision often comes down to a 15-year versus a 30-year mortgage. While the difference may seem simple, your mortgage term directly affects your monthly payment, total interest costs, and long-term financial flexibility.

Understanding Mortgage Term Options

Your mortgage term determines how much you’ll pay each month, how quickly you’ll build equity, and how much you’ll pay in interest over the life of the loan. It also influences your ability to save, invest, and plan for other financial goals along the way.

15-Year Mortgage

A 15-year mortgage allows you to pay off your home twice as fast as a traditional 30-year loan.

Key Features:

- Lower Interest Rates: Shorter terms typically come with lower interest rates, saving you money over time.

- Higher Monthly Payments: Because the loan is repaid in half the time, monthly payments are higher.

- Faster Equity Growth: You’ll build equity more quickly and pay significantly less interest over the life of the loan.

A 15-year mortgage is ideal for buyers who can comfortably manage a higher monthly payment and want to minimize interest costs while reaching full ownership sooner. It’s a strong choice for those focused on long-term savings and financial independence.

30-Year Mortgage

A 30-year mortgage spreads payments over three decades, making it the most popular option for homebuyers seeking affordability and flexibility.

Key Features:

- Slightly Higher Interest Rates: Rates are typically a bit higher than 15-year loans.

- Lower Monthly Payments: Easier to fit into most budgets and ideal for first-time buyers.

- More Financial Flexibility: Lower payments leave room to save, invest, or maintain a comfortable lifestyle while still building equity over time.

A 30-year mortgage works well for buyers balancing multiple priorities—such as saving for retirement, investing, or managing other life expenses—while still achieving homeownership.

Factors to Consider When Choosing Your Mortgage Term

- Monthly Budget

Can you afford the higher payment of a 15-year loan without stretching your finances too thin? If not, a 30-year mortgage may offer more breathing room. - Interest Rates

While 15-year mortgages often have lower rates, the difference can vary depending on market conditions. Always compare current rates before locking in your term. - Homeownership Timeline

If you plan to stay in your home long-term, a 15-year loan can provide major interest savings. However, if you anticipate moving within a few years, the flexibility of a 30-year term might make more sense. - Other Financial Goals

Consider how your mortgage fits into your overall financial plan. If you’re saving for retirement, education, or investments, the lower payment of a 30-year loan could free up funds for those goals.

Smart Strategies for Finding the Right Fit

- Blend the Best of Both Worlds: Choose a 30-year term but make extra principal payments when you can.

- Get Pre-Approved: See what actual rates and payments look like for both options.

- Talk to a Mortgage Expert: A professional can help you evaluate how each term aligns with your broader financial picture.

The Bottom Line

Choosing between a 15-year and 30-year mortgage isn’t just about numbers—it’s about finding the right balance between comfort today and financial confidence tomorrow.

At Standard Mortgage, we’re here to help you explore your options and tailor a loan solution that fits your goals.

Contact us today to get personalized guidance and take the next step toward the home—and future—you deserve.